Savings Plan a Key Factor in Retirement Confidence

The 2015 annual Retirement Confidence Survey (RCS) found that confidence of American workers in their ability to retire comfortably continues to rebound from the record lows of the years 2009- 20013. The key factor in this increasing optimism is having a retirement savings plan in place.

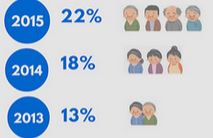

Twenty-two percent of workers are now very confident they will have enough money to live comfortably throughout their retirement years (up from 18 percent in 2014 and 13 percent in 2013). Thirty-six percent say they are somewhat confident. Twenty-four percent of workers are not at all confident that they will have enough money to live comfortably throughout their retirement years (still far above the low of 10 percent in 2007), and 17 percent are not too confident they will have enough money. While nearly half of all workers (49 percent) were not too or not at all confident of having enough money for retirement in 2013, 41 percent report these levels of confidence in 2015

Survey: Having a Retirement Savings Plan a Key Factor in Americans’ Retirement Confidence. EBRI Issue Brief no. 413 (Employee Benefit Research Institute, April 2015).

"Retirement confidence is strongly related to retirement plan participation," said Jack VanDerhei, research director at EBRI. "In fact, workers reporting that they or their spouse have money in a defined contribution plan or IRA or have a defined benefit plan from a current or previous employer are more than twice as likely as those without any of these plans to be very confident (24% with a plan versus 9% without a plan)." Nearly half (46%) of those without a plan were "not at all confident" about their retirement, compared to just 11% of those who do have money in a retirement account.

That's the good news. The not-so-good news is that American workers, particularly those without a retirement account, still have far to go.

The link between retirement accounts and retirement confidence

Perhaps not surprisingly, 9 of out 10 workers participating in a retirement investment plan had set aside money for retirement, compared with just 2 out of 10 of those who don't have a plan. When asked about how much they had in savings and investments (excluding the value of a primary residence), nearly half of respondents with a retirement plan (47%) said they had at least $50,000 set aside; 17% had at least $250,000. By comparison, 73% of workers without a retirement plan had less than $1,000.

In addition, although less than half of all workers had ever tried to calculate how much they will need to retire, those who had money in some sort of a retirement account were twice as likely to have crunched the numbers as those who do not have a plan. And as the RCS demonstrates year after year, calculating a retirement savings goal can lead to retirement confidence.

To save or not to save

Workers seemed to understand the importance of saving for retirement, as 68% said they should be saving at least 10% of their income annually. Sixty-one percent of workers in the 2015 RCS report that they and/or their spouseare currently saving for retirement (up from 57 percent in 2013–2014, but still below the 65 percent measured in 2009)

Worker households with a retirement plan are more likely than those without such plans to report having saved for retirement (90 percent vs. 20 percent.) Not surprisingly, those who do not have a retirement account were more likely to say they needed to set aside at least 50% of their household income for retirement than those with a retirement account. They were also more likely to say they did not know how much they need to save.

So if workers generally understand the need to save and invest, why aren't they doing so?

The reasons they gave include

- the cost of everyday living (53%)

- unemployment or underemployment (14%)

- non-mortgage debt (6%)

- mortgage or housing expenses (5%)

- education expenses (5%).

About the survey

The RCS was cosponsored by EBRI, a private, nonprofit, nonpartisan public policy research organization that focuses on health, savings, retirement, and economic security issues, and Greenwald & Associates, a Washington, DC-based market research firm. The survey was conducted in January 2015 through 20-minute telephone interviews with 1,501 people, including 1,000 workers and 501 retirees. Full results can be viewed at www.ebri.org.

IMPORTANT DISCLOSURES

Material contained in this article is provided for information purposes only and is not intended to be used in connection with the evaluation of any investments offered by David Lerner Associates, Inc. This material does not constitute an offer or recommendation to buy or sell securities and should not be considered in connection with the purchase or sale of securities.

To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances.

These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable– we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Some of this material has been provided by Broadridge Investor Communications Solutions, Inc.

David Lerner Associates does not provide tax or legal advice. The information presented here is not specific to any individual's personal circumstances.

Member FINRA & SIPC.