Smart Retirement Planning: A Real-World Guide to Financial Security

The reality of retirement planning has shifted dramatically in recent years. In 2025, 4.2 million Americans turn 65, a record setting amount.

Despite this milestone moment for millions, confidence in retirement readiness remains surprisingly low. Most Americans don’t feel prepared for retirement. In 2024, 35% felt on track for retirement in contrast to 40% in 2021 per the Federal Reserve

Approaching retirement planning as if you’re cramming for a big test the night before can leave a headache of overwhelming questions and doubt for your financial future.

Yet, it’s never too late to start building a solid foundation, and understanding where you stand at any age can provide the motivation needed to take action.

Social Security: A Foundation, Not A Ceiling

The numbers tell a sobering story. What is particularly striking is the participation gap. Only 64% of non-retirees have a retirement account, like a 401(k), IRA, or defined benefit pension through an employer, and 36% don’t have any retirement savings at all. This could lead to many people heavily relying on Social Security for their retirement income.

Let’s address the elephant in the room. Social Security was never designed to be anyone’s sole source of retirement income, yet for many Americans, it’s becoming exactly that. More than half (52.5%) of Peak Boomers have $250,000 or less in total assets as they approach retirement.

Planning for Reality

Retirement planning extends beyond accumulating a target number. Healthcare costs, inflation, longevity risk, and changing family dynamics all play crucial roles in your retirement success.

Healthcare deserves special attention. Even with Medicare, healthcare costs can consume a significant portion of retirement income. Longevity risk is the possibility of outliving your money. With life expectancies continuing to increase, planning for a 30-year retirement isn’t unreasonable.

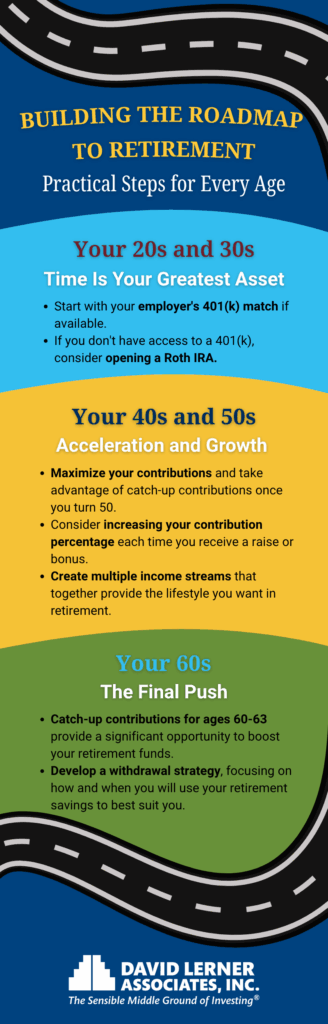

Building the Roadmap: Practical Steps for Every Age

Retirement planning isn’t a one-size-fits-all endeavor, but certain principles apply regardless of your age or income level. The key is to start where you are and build momentum over time.

Your 20s and 30s: Time Is Your Greatest Asset

If you’re in this age group, your greatest advantage is time. Your 20s are arguably the best age to start saving for retirement: The sooner you start saving, the greater potential impact compounding can have on your investments over time.

Start with your employer’s 401(k) match if available. If your company matches 50% of your contributions up to 6% of your salary, and you earn $50,000, contributing $3,000 annually gets you an additional $1,500 from your employer. That’s an immediate 50% return on your contribution.

If you don’t have access to a 401(k), consider opening a Roth IRA.

Your 40s and 50s: Acceleration Time

As you age, your salary may increase, allowing you to contribute a greater percentage of your income to your retirement savings.

This is the time to maximize your contributions and take advantage of catch-up contributions once you turn 50. If you’re behind on savings, consider increasing your contribution percentage each time you receive a raise or bonus.

Your 60s: The Final Push

If you’re in this group and behind on savings, the new enhanced catch-up contributions for ages 60-63 provide a significant opportunity to boost your retirement funds.

This is also the time to develop a withdrawal strategy, focusing on how and when you will use your retirement savings to best suit you.

The goal is to create multiple income streams that together provide the lifestyle you want in retirement.

An investment counselor can act as a guide for these life-changing decisions. They can help establish goals, navigate long-term investment options, and implement a suitable retirement plan. You can speak to an investment counselor at David Lerner Associates to assess your retirement needs.

The Path Forward: Making It Personal

The data and strategies outlined here provide a framework, but your retirement plan needs to reflect your unique circumstances, goals, and values. Some people prioritize early retirement and are willing to live more frugally to achieve it. Others prefer to work longer and maintain a higher standard of living throughout their lives.

“The key to successful retirement planning isn’t just about hitting target numbers,” says John Fielding, Senior Vice President, Investments at David Lerner Associates, Inc. “It’s about creating a personalized strategy that adapts to your life changes while maintaining the discipline to stay committed to long-term goals, even when market volatility or life circumstances tempt you to veer off course.”

The most important step is to begin. Your retirement story doesn’t have to end with financial stress or dependence on others. With the right combination of employer-sponsored accounts, IRAs, Social Security optimization, and consistent saving habits, you can build a retirement that provides both financial security and peace of mind.

Material contained in this article is provided for information purposes only. It is not intended to be used in connection with the evaluation of any investments offered by David Lerner Associates, Inc. This material does not constitute an offer or recommendation to buy or sell securities and should not be considered in connection with the purchase or sale of securities. These materials are provided for general information and educational purposes, based on publicly available information from sources believed to be reliable. We cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice. The subject of this article is fictitious and created for illustrative purposes only. It is based on events of a similar nature and should not be interpreted as a direct depiction of any specific individual, organization, or incident. Any resemblance to actual persons, living or deceased, or actual events is purely coincidental.