The Retirement Spending Smile

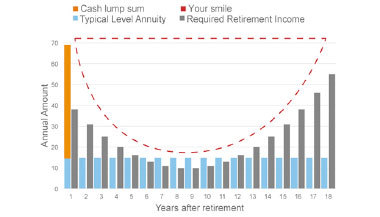

Most people assume that once you retire, your spending pattern will be the same year-to-year. Research has shown that this, in fact, is not the case. Two studies came to the same conclusion. We spend more at the beginning of retirement and again towards the end. The graph of a retiree’s spending pattern looks like a big smile.

Knowing what to do with your money once you retire is just as important as saving enough to retire on. Three in four respondents to a survey did not know how much they can safely withdraw from savings every year, according to an Ipsos survey for New York Life. This survey polled more than 800 people, ages 40 and older with incomes and assets of at least $100,000 — a segment of the population we expect should be relatively well informed on financial matters — but the study found that there is widespread confusion about how and when to draw down retirement savings.

Retirement spending tends to run in three phases:

The Early Years: This is the time you’re more likely to take vacations, go on cruises, and spend time doing all those interesting things you always wanted to do.

Settling In: As the years go by you become less active and spend less time out and about. The spending curve drops down and evens out at the bottom of the smile curve for a number of years.

Final Phase: The cost of healthcare, and the need for assistance increases. If you have to pay for a retirement home or frail care, that pushes the expenditure curve way up again. As you can see from the graph the final phase is even higher than the early stages of retirement.

So, there is no exact number of how much to draw out of your retirement fund each year. It will depend on how much you have in the nest egg and what your “smile” looks like. Calculate what you think you’ll need each year, and see if you’ll have enough to last all the years of your retirement.

IMPORTANT DISCLOSURES

Material contained in this article is provided for information purposes only and is not intended to be used in connection with the evaluation of any investments offered by David Lerner Associates, Inc. This material does not constitute an offer or recommendation to buy or sell securities and should not be considered in connection with the purchase or sale of securities.

To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law.

Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances.

These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable– we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

David Lerner Associates does not provide tax or legal advice. The information presented here is not specific to any individual's personal circumstances. Member FINRA & SIPC