David Lerner Associates: Does it Cost More to be a Woman in 2015?

Many areas of women’s lives are in the spotlight during International Women’s month. One important factor that has still not been achieved in the US is financial equality – as witnessed by the responses to Patricia Arquette’s passionate plea for equal pay for equal work in her acceptance speech at the 2015 Oscars.[1]

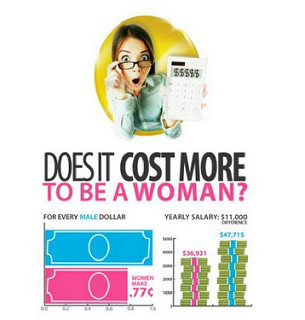

Does it cost more money to be a woman in the U.S. today than it does to be a man? A study conducted by the FINRA Education Institute suggests that in a couple of areas, at least, the answer may be yes.

According to the U.S. Census Bureau, women still tend to lag behind men when it comes to compensation. Women today earn an average of 77 cents for every dollar earned by a man,—resulting in an annual salary difference of more than $11,000.

In a recent interview Sheryl Sandberg, COO of Facebook and author of the best-selling book Lean In, addressed the critics of this statistic. The pay gap is undeniably real, said Sandberg. Even if one takes into account the differences in number of hours and years worked, women are still paid less than men and women deserve to get paid the same for the same jobs.

Financially-speaking there are other areas where women are at a disadvantage: women pay a half-point higher interest rate on credit cards than men do, according to the FINRA study. Over a lifetime, this could add up to thousands of more dollars spent by women in interest charges than is spent by men.

The FINRA study determined that women with low levels of financial literacy tend to be more vulnerable to credit card mismanagement than are men with comparable levels of financial literacy. For example, these women are more likely to carry a balance on their cards, to make only the minimum payment each month, and to pay late fees.

Financial Literacy Lessens the Blow

When men and women with high levels of financial literacy are examined, the gender differences with regard to credit card management disappear. Education could be more of a factor in the difference between credit card management practices between men and women than policy. In fact, FINRA states that improving financial literacy may improve women’s credit card behavior by 60 percent more than men’s credit card behavior.

According to the U.S. Census Bureau, women across all age groups are about four times more likely to become widows than men are to become widowers. Therefore, it may be especially important for women to improve their financial literacy. Women may want to concentrate their financial literacy efforts in these three areas:

1. Know your spending patterns. A basic budget will show you what your income is, what your expenses are, and where the money you spend is actually going. It may also help you prioritize your spending, including contributing to a retirement savings plan like a 401(k) or Individual Retirement Account (IRA).

2. Keep your financial paperwork organized. Overstuffed file folders and shoeboxes filled with receipts may not be an adequate recordkeeping system for many women today. Consider setting aside a day (or a weekend or longer, if necessary) to work on getting your finances in order.

3. Invest wisely. No single investment strategy is right for every woman, which makes it important to understand the basics of investing so you can formulate the right strategies for you. Therefore, you may want to consider working with a personal investment counselor, who can make recommendations based on your specific goals, time frame and risk tolerance.

Download the infographic from Slideshare

IMPORTANT DISCLOSURES

Material contained in this article is provided for information purposes only and is not intended to be used in connection with the evaluation of any investments offered by David Lerner Associates, Inc. This material does not constitute an offer or recommendation to buy or sell securities and should not be considered in connection with the purchase or sale of securities.

These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable– we cannot assure the accuracy or completeness of these materials.

David Lerner Associates does not provide tax or legal advice. The information presented here is not specific to any individual's personal circumstances. Member FINRA & SIPC.