David Lerner Associates: Your Credit Profile

Your credit profile can make a big difference in your financial life, not only for a major purchase like a home or car, but also for college loans, credit card terms and insurance premiums. It might even come into play when you rent an a artment or apply for a job. That's why .it's important to be familiar with your credit score and your credit report.

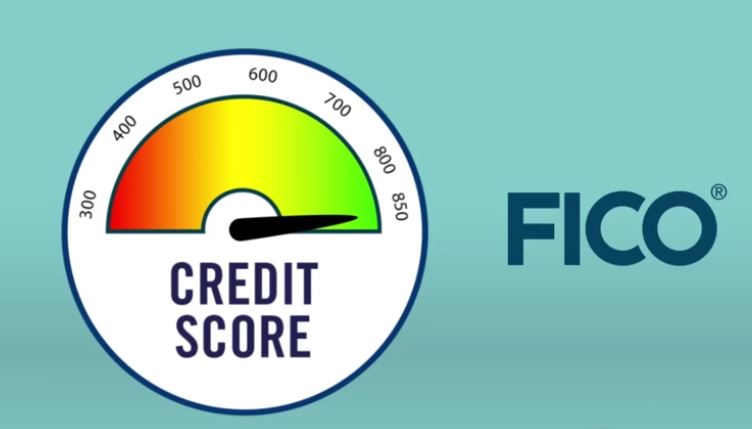

The most common score is your FICO score- a three-digit number that ranges from 300 to 850. What;s a good score? that can vary by lender and situation.If your socr ein 700 or higher you may be eligile for favorable terms fomr lenders and fnancial srvices companies. If your score is below 700 you may have to pay a premium for credit. Below 620 you could have trouble getting a oan at all.

Until recently you had to pay to see yuor cedit score. NOw, thatnks to the Consumer Financial Protection Bureau, millions of AMericans have, or will have, free access to their credit scors through their credit card companies. They next time you get your monthly credit card statement look for your credit score. Or you can check your account on the company's website.

How is your score determined? the three major credit reporting agencies – Experian, Equifax and Transunion – keep track of your credit history and assgn you a corresponding credit score, typcially using software develioped by Fair Isaac Corporation or FICO. A mistake on your credit history can negatively affect your score. so it's important to monitor you report periodically. You can order a free credt report annually from each of the three reporting agencies.

Over the next six to 39 months consumers can expect additional credit protections. thanks to a March 2015 settlement between the three agencies and the state of New York. Speciifally, consumrer who are disputing their credit reports wil lbe able to receive a second free report from each agency. Ech agenc must have trained personnel examine documentation from both the cosumer and the lender and make a reasoned judgement, rather than simply accepting the lender's version of events.

Each ageny must wait 180 days before dding medical debt to a credit report.and must remove medical debt from a report when the debt has been paid by an insurance company.

If your credit score is lower than you expect, or even if ou have a high score, it's a good idea to obtain your report for each agency on a regulalr basis and make sure that all versions are correct. YOu can order your free credit reports at www. annualcreditreport.com or by calling 877-322-8228.