New Rules of Financial Independence: What Gen Z Graduates and Their Parents Need to Know

Graduation is often framed as a beginning. But financially, it’s something more consequential: a turning point.

A new graduate pivots to a new phase of life, one that includes earning income, making independent decisions, and, perhaps most importantly, establishing patterns that can shape their financial life for decades. While most advice at this stage focuses on budgeting and paying bills, that’s only part of the story.

The real opportunity during the first few years after graduation is not only learning how to manage money. It’s also learning how to build wealth wisely.

For parents, this moment carries equal weight. According to a 2026 Wells Fargo study, two-thirds (64%) of parents with Gen Z children ages 18 to 28 say their children rely on them financially, whether for money, housing, or other support. More than half of those parents say that support is straining their own finances.

Almost half of Gen Z respondents (46%), describe their financial lives as “messy”, and many say they are postponing their future goals such as relocating, getting married, pursuing education, and career changes.

The question is no longer whether to help, but how to help in a way that builds confidence rather than dependence.

This guide is designed to do both: offer graduates a path forward, and help families navigate this transition with clarity, structure, and intention.

Why Financial Independence Looks Different in 2026

The traditional post-graduation roadmap may have felt predictable: secure a full-time job, follow a steady career ladder, and gradually build financial stability.

That model of the American Dream may be shifting.

Today’s graduates are entering a workforce shaped by uncertainty and rapid change. Entry-level roles are more competitive than they’ve been in decades, and many of the positions that once served as steppingstones are being reshaped or replaced by automation and AI.

Additionally, many Gen Z workers are not relying on a single source of income. Instead, they are building financial lives that include side work, freelance projects, or multiple part-time roles. For them, income diversification is not a fallback; it’s a strategy.

But this shift can come with trade-offs.

Irregular income makes consistency harder. Benefits like retirement contributions and health insurance may no longer be “built-in” to the work trajectory. And without the structure of a traditional paycheck, the responsibility to save and invest becomes entirely self-directed.

In this environment, financial independence is less about stability and more about adaptability.

The Emotional Side of Money

What’s often missing from financial advice is the emotional reality behind it.

Many graduates are navigating not just financial decisions but also financial anxiety around job security, rising costs, and whether they are “on track” compared to their peers. At the same time, parents watching from the sidelines can often feel a mix of concern and responsibility.

This creates a dynamic that is rarely discussed but deeply important: the emotional contract between parents and their adult children.

When financial support is involved, clarity matters. Is the support a short-term bridge or an open-ended safety net? Is it a gift or a loan? What milestones signal independence?

Without clear communication, both sides can feel strained. Graduates may carry guilt. Parents may feel uncertain about their own financial future.

However, when handled thoughtfully, these conversations can become a source of strength, building trust, accountability, and shared understanding.

Rethinking the Standard Financial Advice

Advice given to graduates today may look different than the standard advice that was given decades ago.

Take career paths. Job-hopping was once seen as risky. Today, it is often one of the most effective ways to increase income. Side hustles were once uncommon; now they are a core part of many financial strategies.

Even long-standing debates, like renting versus buying, require a more nuanced view. Flexibility, mobility, and timing now matter as much as ownership. Yet, while many rules have changed, one principle has not: time remains the most powerful force in building wealth.

Starting early, even with small amounts, can have an outsized impact over time. The graduate who begins investing at 22 has a meaningful advantage over one who waits until 32. Not because they save more, but because their money has more time to grow.

Parents as Financial Coaches—Not Financial Backstops

For parents, the instinct to provide support is natural. But the form that support takes can shape outcomes for years to come. The most effective role is not that of a financial backstop, but of a financial coach.

This means helping graduates think through decisions rather than solving them. It means encouraging structure, how income is allocated, how savings are built, and how debt is managed without removing responsibility. Try sharing financial literacy tips gradually, discussing smart money tactics and explaining personal, early career learning curves.

Being in the support role also means setting clear boundaries. Support works best when it is defined: what it covers, how long it lasts, and what progress is expected along the way. This clarity protects both the graduate’s independence and the parent’s long-term financial security.

In fact, many parents today are balancing two priorities simultaneously: helping their children while ensuring they remain on track for their own retirement. A coaching mindset allows both goals to coexist.

Closing the Financial Literacy Gap

Behind many of these challenges is a quieter issue: a gap between access to information and true financial understanding.

Gen Z has unprecedented access to financial content, much of it through social media. But accessibility does not always translate into depth, context, or personalization.

Understanding how to build wealth requires more than general advice. It requires applying principles to specific situations: income variability, debt levels, risk tolerance, and long-term goals.

This is where guidance becomes valuable.

Graduates who make the most progress early on are not always the ones with the highest salaries. They are the ones who begin organizing their finances early—often imperfectly—and who develop consistent habits around saving, investing, and decision-making.

Financial literacy, in this sense, is not just knowledge. It’s behavior.

Remember that post-grad financial literacy doesn’t come all at once. It’s also okay to figure things out as you go, that’s what early adulthood is often all about.

A Practical First-Year Financial Framework

For graduates stepping into financial independence, the goal is not perfection. It’s momentum.

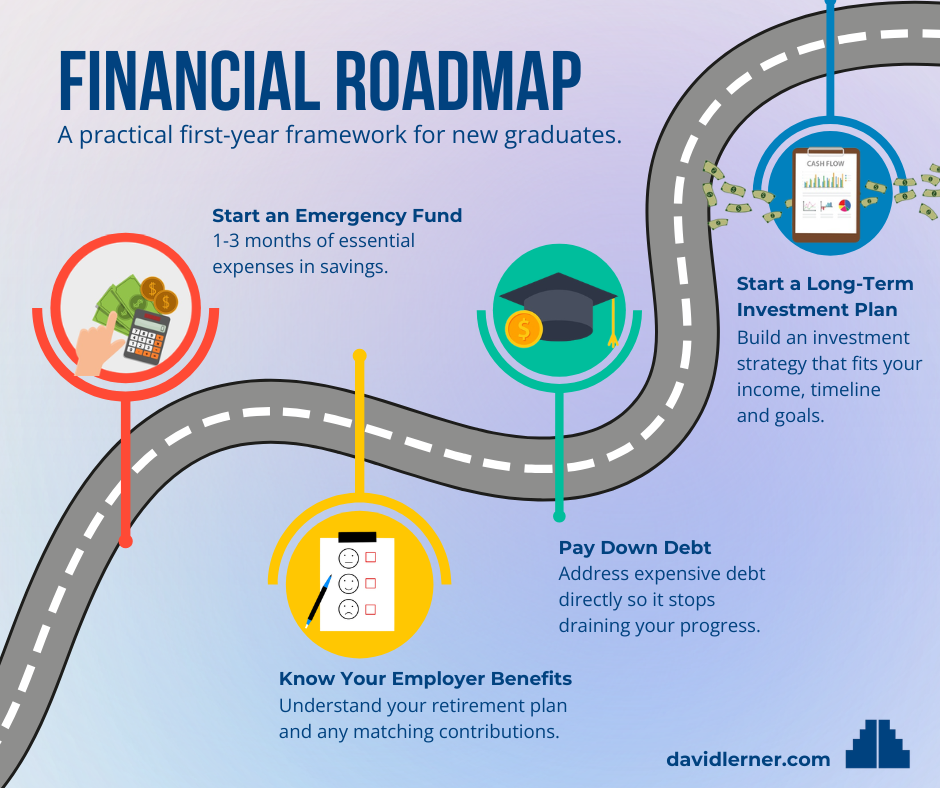

A clear starting point includes:

- Building an emergency fund, even a modest one, to create stability

- Understanding and maximizing any employer retirement benefits

- Addressing high-interest debt with a structured plan

- Beginning to invest early, with a long-term perspective

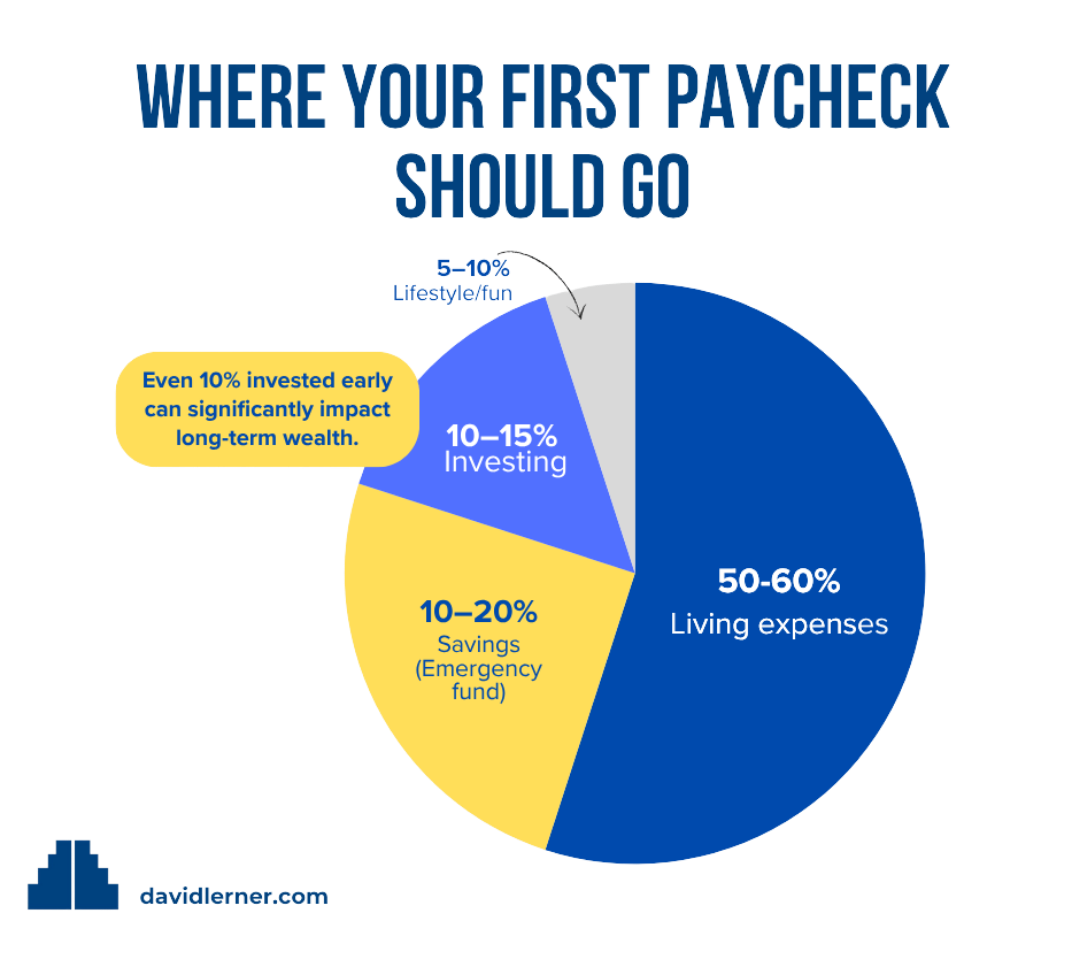

After establishing the different places, you want your income to go, you can weigh how much of your paycheck you want to go to each. This can differ based on circumstances, but a general framework can look like this:

These steps are not complicated, but they are foundational. Because in today’s environment, certainty rarely comes first. Progress does.

And the habits formed in this first year: how money is managed, how decisions are made, how risks are approached, tend to compound over time, just as powerfully as any investment.

For Parents and Young Adults: Navigating Post-Grad Together

Financial independence today does not look like it did a generation ago.

It is less linear, less predictable, and more self-directed. But it also offers something different: the opportunity to build a financial life that is flexible, intentional, and aligned with changing realities.

For graduates, the focus should not be on getting everything right immediately. It should be on starting early, building habits, and staying engaged. For parents, the opportunity is to guide without overstepping. To support in ways that empower rather than replace independence.

Because ultimately, financial success in this new landscape is not defined by a single decision. It is built, steadily, deliberately, over time.

Material contained in this article is provided for information purposes only. It is not intended to be used in connection with the evaluation of any investments offered by David Lerner Associates, Inc. This material does not constitute an offer or recommendation to buy or sell securities and should not be considered in connection with the purchase or sale of securities. These materials are provided for general information and educational purposes, based on publicly available information from sources believed to be reliable. We cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.