Financial Independence in Retirement: How to Turn Savings Into Reliable Income

Sarah and Jeff had done everything right.

They had saved consistently for 30 years, put heavily into their contributions when they could, and resisted the temptation to cash out during the rough patches. By the time Jeff turned age 58 and Sarah age 56, their combined retirement accounts sat at just over $1 million. They had hit the number they had been aiming for since their late twenties.

The conversation of retirement was becoming realer by the day. So why didn’t they feel ready?

On paper, the balance looked solid. But when they tried to work out what their actual monthly income would be in retirement, the math kept falling apart. Everything they had was invested for growth. To pay the bills, they would need to sell. And selling meant making the right call at the right time, every single time, for the next thirty years.

“We have the money,” Jeff told Sarah. “I just don’t know where the monthly income is going to be coming from.”

That money conversation, unremarkable on its surface, turned out to be one of the most important ones. Because what Jeff said points to a gap many retirement plans never properly address: how to turn savings into income.

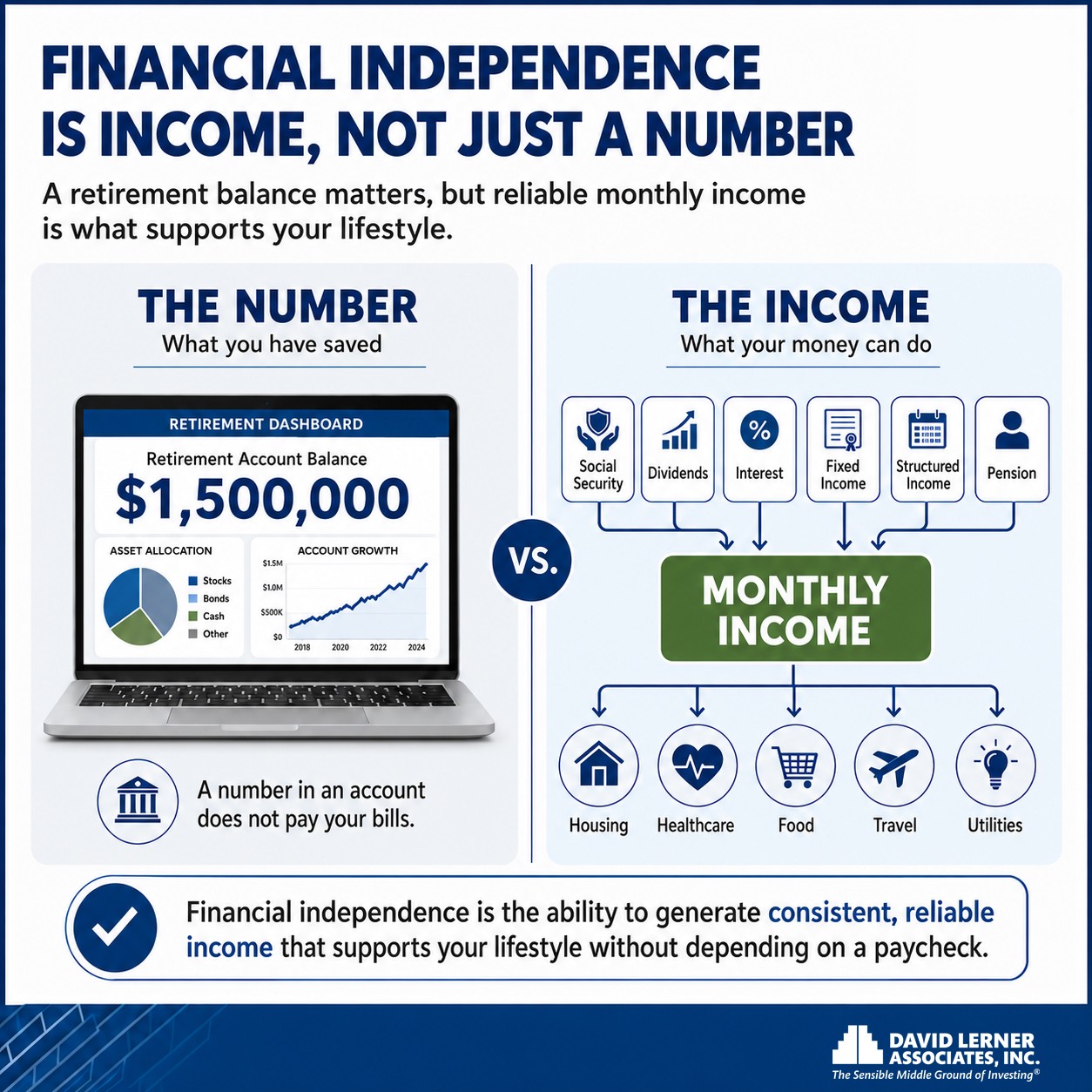

Retirement Planning is More than Just a Number to Aim For

Most people spend their working lives chasing a number. A million dollars. Two million. Whatever figure feels enough to be secure but still achievable. But a number in an account does not pay your bills. Income does. And understanding that distinction is where real retirement planning begins.

Most people spend their working lives chasing a number. A million dollars. Two million. Whatever figure feels enough to be secure but still achievable. But a number in an account does not pay your bills. Income does. And understanding that distinction is where real retirement planning begins.

“Individuals who arrive at retirement with the most confidence are not necessarily the ones who accumulated the most,” says David Beckerman, Senior Vice President, Investments at David Lerner Associates.

“They are the ones who converted accumulation into a sensible middle-ground of investing. They know what their income is. They know where it is coming from. That clarity is what financial independence can actually feel like.”

What Financial Independence Actually Means for Retirement

Financial independence is not a moment in time, but countless actions and choices that build towards greater control over your money and life. There is no definitive value amount that can guarantee it, just as there is no single path that leads everyone there.

In reality, financial independence is the ability to generate a consistent, reliable income that supports your lifestyle without depending on a paycheck.

That shift in focus from “how much do I have?” to “how much can I count on?” changes how you approach long-term planning.

Contributing is Not the Same as Planning

According to a recent Vanguard Retirement study, only about 4 in 10 Americans are on track to maintain their standard of living in retirement. Workers with access to workplace Defined Contribution plans (like 401ks) are almost twice as likely to be on track than those without.

Access to a retirement plan matters, but it’s only the starting point. What separates those who feel genuinely secure isn’t the size of their balance. It’s whether that balance has been converted into reliable income. They’re the ones who know exactly what’s coming in every month beyond market volatility.

The Problem With “Accumulate and Withdraw”

The conventional retirement model is straightforward: save as much as possible, maximize returns during your working years, and when you retire, start withdrawing. But it carries a vulnerability that many investors may not understand until they are living it: the lasting risk of withdrawing during market downturns.

Morningstar’s 2025 State of Retirement Income report found that there was high risk of exhausting retirement savings when market returns were poor in the first five years of retirement.

This is the dilemma of the “sequence-of-return risk”: if markets decline significantly in the first few years of retirement and you are simultaneously withdrawing from that portfolio to fund your lifestyle, the damage becomes far harder to recover from than during your accumulation years.

You are not riding out a downturn. You are selling into one, at the worst possible moment, locking in losses that could have permanent impacts on your retirement.

Portfolios with higher volatility, such as those with heavy equity allocations, are often associated with lower safe withdrawal rates, because greater market swings increase exposure to sequence-of-returns risk at the worst possible time.

For retirees and pre-retirees exploring paths to financial independence, building reliable monthly income into a long-term plan, rather than depending solely on portfolio withdrawals, can be one of the most practical steps toward protecting retirement security.

What an Income-Focused Plan Looks Like

An income strategy is not one thing. It is several complementary income streams working together, calibrated to your timeline, your tax situation, and the lifestyle you want to sustain.

In practice, this typically involves a combination of dividend-paying investments that generate regular cash flow, interest-generating fixed income securities that provide stability and predictability, structured income strategies tied to your specific retirement timeline, and in some cases, insurance-based income solutions that can guarantee a floor of income regardless of market conditions.

The goal is not to abandon growth. A retirement that lasts 25 or 30 years still requires a portfolio that keeps pace with inflation. The aim is to make sure that growth does not have to do all the heavy lifting. When income is built in, you have more flexibility to let growth assets ride through volatility without being forced to liquidate them at the wrong moment.

When to Make the Investment Strategy Shift

One of the most consequential and underappreciated transitions in retirement planning is the move from accumulation to income. During your working years, growth is a main priority. That make sense when further you are from retirement, the more time you have to recover from market downturns, and the more aggressively you can afford to invest.

But as retirement approaches, the picture changes. The risk profile that made sense at age 45 may expose you to risk that doesn’t align at age 62. The shift toward income generation, capital protection, and inflation-adjusted cash flow can begin gradually, deliberately, and well before the day you stop working.

Waiting until retirement to begin thinking about income can be one of the most common and costly planning mistakes. It requires intentional and proactive planning that factors in your current portfolio, time horizons and what you will need to live comfortably in retirement.

Income Questions Worth Asking Now

Financial independence planning does not have to be overwhelming. Try breaking it into clear, practical questions:

- What does your lifestyle actually cost? Not a rough estimate — a real monthly number that accounts for housing, healthcare, travel, and the spending patterns you expect to carry into retirement. That figure is your baseline.

- What reliable income sources do you already have in place? This can include Social Security, pension income, and current investment income. Many overestimate the ability of one income source to cover their expenses. Add them up honestly with tangible numbers in mind.

- Where are the income gaps? The difference between what you have and what you need gives a more realistic sense of where to focus your planning.

- How much risk are you comfortable with having in your portfolio?

- Is your strategy able to withstand unexpected costs and a retirement period that could last beyond age 90?

Stress-testing a plan before it is needed is far less disruptive than discovering its limits after the fact.

Creating Financial Independence

Financial independence is not a milestone you hit once. It is a foundation you build, carefully and intentionally, with the right income strategy at its center. The number in your account matters. But reliable income is what turns that number into a plan you can actually live on.

Looking to map out your financial independence plan? Consider talking to an Investment Counselor at David Lerner Associates, Inc. We can help evaluate your strategy for retirement and find ways to align to your goals.

Material contained in this article is provided for information purposes only. It is not intended to be used in connection with the evaluation of any investments offered by David Lerner Associates, Inc. This material does not constitute an offer or recommendation to buy or sell securities and should not be considered in connection with the purchase or sale of securities. These materials are provided for general information and educational purposes, based on publicly available information from sources believed to be reliable. We cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.The subject of this article is fictitious and created for illustrative purposes only. It is based on events of a similar nature and should not be interpreted as a direct depiction of any specific individual, organization, or incident. Any resemblance to actual persons, living or deceased, or actual events is purely coincidental. David Lerner Associates does not provide tax or legal advice. The information presented here is not specific to any individual’s circumstances. Each taxpayer should seek independent advice from a tax professional based on his or her circumstances.